How Do You Properly Endorse a Personal Check?

If you have ever shown up to cash a personal check and gotten a surprise “no,” odds are it was something simple on the back of the check. This guide walks you through how to properly endorse a personal check so you can avoid the most common, totally preventable issues.

Endorsement rules can vary a bit depending on where you cash it, but the mistakes that cause problems are usually the same. People sign too early, sign outside the endorsement area, use a name that does not match their ID, or accidentally write “for deposit only” and limit what can be done with the check.

We will also cover what to do when a check is made out to two people, plus why torn, taped, smudged, or altered checks get extra scrutiny.

Where Do You Endorse a Personal Check?

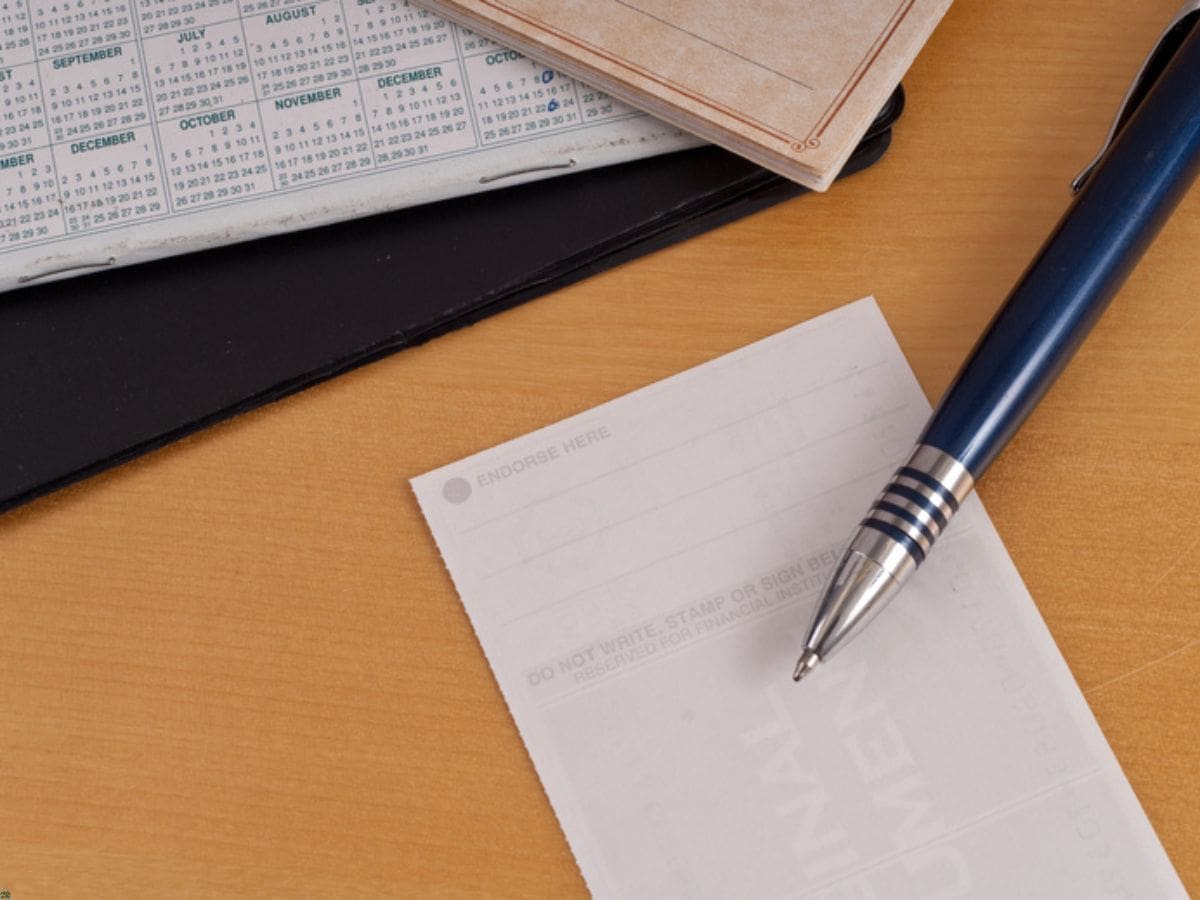

Flip the check over and find the endorsement box, usually near the top and marked “Endorse Here.” That box is the only place you should sign, and keeping the signature inside the lines helps us verify it quickly.

When you endorse a personal check with us, your signature should match the payee name on the front as closely as possible. If the check is made out to “Michael A. Smith,” sign “Michael A. Smith,” not a nickname or shortened version.

- Sign only inside the endorsement box.

- Keep it legible and avoid extra notes or marks.

- Do not correct or cross out your signature.

If you are unsure whether your name format will match your ID, wait to sign until you are at our location. We can review it with you first so you do not accidentally create a mismatch that slows everything down.

How Do You Endorse a Personal Check for Cashing?

Use a Blank Endorsement When You Plan to Cash It

For check cashing, the simplest approach is a blank endorsement, which means signing your name as printed on the front of the check. Chase notes that signing in the endorsement area is the common method, and it also highlights that restrictive wording can limit how a check is processed.

Keep It Simple

- Sign only your name, written clearly.

- Skip added phrases like “for deposit only” if you want cash.

Only Add Extra Details If We Ask

Sometimes we may request a phone number or an ID reference to help verify the transaction. Add only what we request, and keep everything neat so it stays readable.

If you are unsure whether you should write anything beyond your signature, ask us first. A clean endorsement is easier to verify and less likely to trigger delays.

The Biggest Endorsement Mistakes That Get Checks Rejected

Mistakes That Create Instant Verification Problems

Signing too early can raise risk because the endorsement is what turns a check into something another person could try to use. KeyBank points out that proper endorsement is a security step that helps reduce fraud risk, which is why timing and clarity matter.

Name and ID Mismatches We See a Lot

- Using a nickname when the check is written to a legal name.

- Leaving off a middle initial or suffix like Jr. or Sr. when your ID includes it.

- Signing with a stylized signature that does not resemble your ID name at all.

Messy Endorsements That Slow Everything Down

Scribbles, crossed-out signatures, signing twice, or writing in multiple places can make a check look altered. If you are cashing with us, the safest move is to keep it clean, sign once, and make sure the endorsement matches the payee and your ID so verification stays simple.

What Does For Deposit Only Mean, and Why Can It Stop Check Cashing?

What a Restrictive Endorsement Does

Writing “for deposit only” is a restrictive endorsement that tells the payment system the check should go into an account, not be exchanged for cash. The CFPB explains that this wording plus your signature limits the check to deposit into your account.

Why It Can Block Over-the-Counter Cashing

- It can conflict with check-cashing processing because it signals deposit-only handling.

- It may force a “no” even if everything else on the check looks fine.

If You Already Wrote It

If you plan to cash with us and you already added restrictive wording, pause before adding anything else.

- Call us to confirm our policy for that situation before you come in.

- If needed, contact the issuer and request a replacement check.

The key is not trying to “fix” it by scribbling over the endorsement, since that can make the check look altered. A quick policy check with us usually saves a wasted trip and keeps your options open.

How Do You Endorse a Check Made Out to Two People?

Read the Payee Line Before Anyone Signs

The word between the two names is the whole game. The CFPB notes that when a check is written to two people with “and,” both payees generally need to sign, while “or” can allow either person to endorse.

Quick Examples

- John and Jane: plan on both people being involved.

- John or Jane: one person may be able to handle it, depending on requirements.

How We Avoid Wasted Trips

- Bring both payees and matching IDs when the check uses “and.”

- Call us first if one person cannot be present so we can tell you what will and will not work.

If the wording is unclear or the names are tight to read, do not guess and do not sign yet. We would rather review it with you first than have you make an endorsement that creates unnecessary limits.

What If the Check Is Torn, Taped, Smudged, or Looks Altered?

Why Condition Matters for Approval

A torn or altered check can slow verification because we have to confirm the details are readable and unchanged. The Federal Reserve’s Regulation CC resources cover check collection and warranties, which is one reason providers pay close attention to checks that appear damaged or modified.

Red Flags We See Most Often

- Torn corners or a ripped edge that clips the routing, account, amount, or payee line.

- Tape over key areas, especially if it crosses numbers or the payee name.

- Smudged ink or water damage that makes characters hard to confirm.

- Heavy corrections or overwriting that suggests the check details were changed.

Best Next Step

If anything looks questionable, the cleanest fix is usually asking the issuer for a reissued check. When you bring us a check that is intact and easy to read, we can process it faster and with fewer questions.

A Quick Checklist Before You Cash It

The safe play is simple: endorse in the correct box, sign your name the way it appears on the front, and skip restrictive wording if you want cash. If two names appear on the payee line, read the “and” or “or” carefully so you do not get stuck needing an extra signature at the last minute.

Before you come see us at DNV Cheques, wait to sign until you are ready, bring valid ID that matches the payee name, and make sure the check is clean, readable, and unaltered. Those three steps prevent most avoidable delays and help us move your transaction along smoothly.